Arizona Long Term Care Insurance: What Retirees Should Know

Long-term care costs in Arizona are climbing faster than most retirees expect, and without a plan, these expenses can drain your savings quickly.

We at Signature Senior Solutions LLC help Arizona retirees understand their options so they can protect their assets and maintain their independence. This guide walks you through the types of coverage available, how to evaluate what fits your situation, and the practical steps to move forward with confidence.

What Long-Term Care Insurance Actually Covers

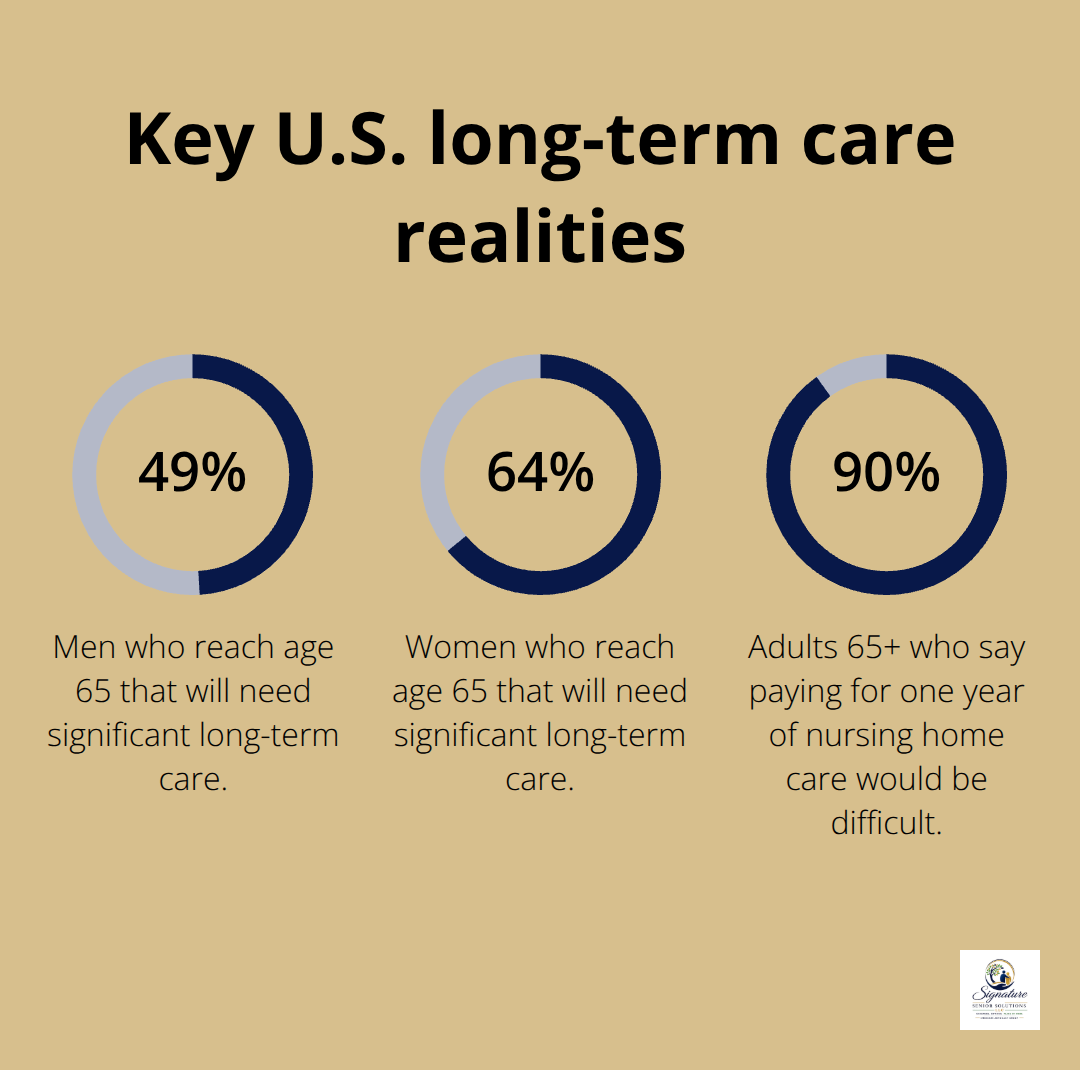

Long-term care insurance pays for services Medicare won’t touch-assistance with daily activities like bathing, dressing, and eating, plus memory care if cognitive decline sets in. This coverage works in nursing homes, assisted living facilities, or your own home, depending on your policy and needs. According to the U.S. Department of Health and Human Services, about 49% of men and 64% of women who reach age 65 will need significant long-term care at some point. Without this insurance, you’ll face costs that most Arizona retirees severely underestimate.

A Kaiser Family Foundation survey found that 90% of adults 65 and older say paying for even one year of nursing home care would be difficult. That’s not pessimism-it’s realistic. In Phoenix, skilled nursing costs about $10,589 per month in 2026, according to the LTC News Cost of Care Calculator. In Tucson, you’re looking at roughly $10,562 per month. These numbers climb annually, and they represent just one type of care. Assisted living in Phoenix runs around $4,968 per month, while in-home care for 44 hours per week costs approximately $7,194 per month. The financial gap between what Medicare covers and what you’ll actually need is enormous.

Why Medicare and Medicaid Fall Short

Medicare covers only limited skilled care immediately after hospitalization-typically 100 days maximum, and only if you meet strict conditions. After that, you’re on your own. Medicaid can eventually pay for long-term care, but only after you’ve spent down your assets to roughly $2,000 for individuals under Arizona’s ALTCS program, as detailed by AHCCCS. That means years of paying full price out of pocket before Medicaid kicks in, which drains retirement savings meant for your spouse, heirs, or your own quality of life.

Long-term care insurance fills this gap by covering the activities of daily living and cognitive decline that Medicare explicitly excludes. This protection lets you access care without depleting decades of savings first.

Arizona’s Partnership Program Advantage

Arizona participates in the Long-Term Care Partnership Program, which offers dollar-for-dollar asset protection when you hold a qualified policy. For every dollar your policy pays in benefits, you can protect an equal amount of assets if you later qualify for Medicaid. This feature alone makes planning with insurance far smarter than hoping Medicaid will save you later. The Partnership Program also includes reciprocity with other states, so asset protection can follow you if you move.

Why Your Age Matters More Than You Think

Starting your search in your 50s locks in substantially lower premiums than waiting until 60 or beyond. A 55-year-old typically pays far less per month than a 65-year-old for identical coverage, and your health status won’t have declined yet, making approval easier and options broader. Health conditions that develop later can make traditional policies unattainable or prohibitively expensive. The cost difference between starting at 55 versus 65 often justifies the premium payments themselves.

Understanding what long-term care insurance actually covers sets the foundation for evaluating which type of policy works best for your situation and budget.

What Long-Term Care Coverage Options Exist for Arizona Retirees

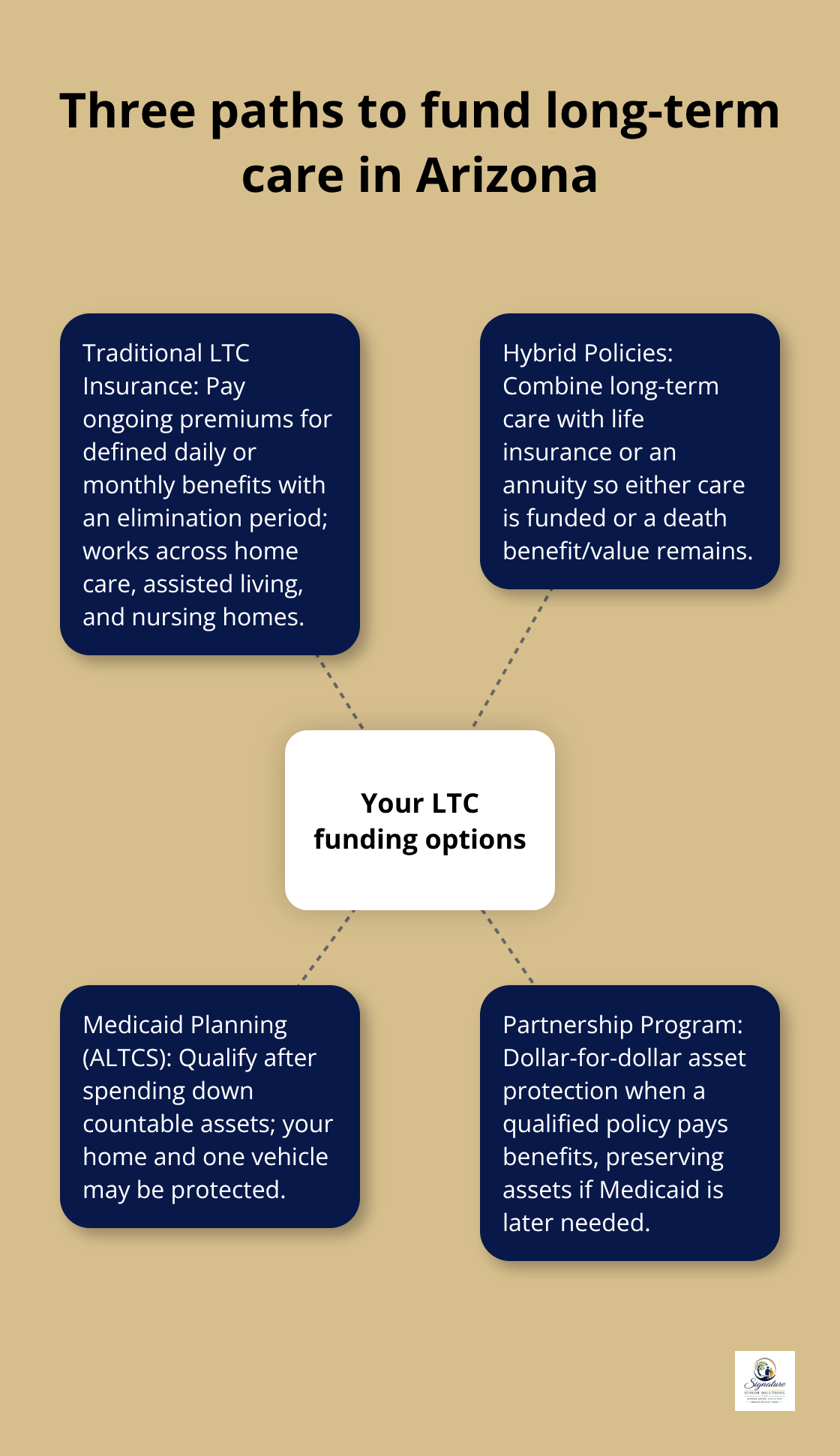

Traditional Long-Term Care Insurance Policies

Arizona retirees can purchase traditional long-term care insurance by paying a monthly premium in exchange for coverage when care needs arise. The policy reimburses covered services up to your daily or monthly benefit limit. According to the National Association of Insurance Commissioners, traditional policies covered about 6.1 million Americans in 2022, making them the most common choice. In Arizona, you can select daily benefit amounts ranging from $100 to $300 or higher, with benefit periods stretching from 3 years to lifetime coverage. The elimination period-the waiting time before benefits start-typically runs 90 days, though shorter and longer periods exist.

Inflation protection matters significantly in Arizona because costs rise roughly 3% annually. A policy purchased today will cover substantially less in 15 years without this rider. Premium costs depend heavily on your age and health status. A healthy 55-year-old in Arizona might pay $1,200 to $2,000 annually for solid coverage, while a 65-year-old typically pays $2,500 to $4,500 for the same benefits. The downside is that historically, 70% to 80% of traditional policy holders faced premium increases over time, according to the American Association for Long-Term Care Insurance, which frustrates many retirees who budgeted based on initial rates.

Hybrid Life Insurance and Long-Term Care Policies

Hybrid policies, also called linked-benefit plans, bundle long-term care coverage with life insurance or annuities, and they’ve grown significantly in popularity. The National Association of Insurance Commissioners reported that about 900,000 Americans held hybrid policies in 2022. These products appeal to retirees who worry about never using long-term care benefits and want their premiums to deliver value either way. If you don’t use long-term care benefits, your heirs receive a life insurance payout or an annuity continues paying. If you do need care, the policy covers it, though the death benefit or annuity value shrinks by the amount paid for care.

Hybrid policies cost more upfront-typically 30% to 50% higher than traditional coverage-but they eliminate the feeling of wasted premiums if you never need long-term care. This trade-off appeals to retirees who prioritize legacy planning alongside care protection.

Medicaid Planning and Asset Protection in Arizona

Medicaid planning and asset protection represent a third path, and it’s the one most Arizona retirees misunderstand. Under Arizona’s ALTCS program, you can qualify for Medicaid-funded long-term care after spending down assets to $2,000 for individuals, though your home and one vehicle remain protected. The five-year look-back period means Medicaid scrutinizes asset transfers made within five years before you apply, so gifting money to children won’t work.

The real advantage lies in Arizona’s Long-Term Care Partnership Program: if you own a qualified long-term care insurance policy and later exhaust those benefits, you can protect additional assets equal to what your policy paid out before Medicaid coverage begins. This combination-insurance plus Medicaid planning-preserves far more wealth than relying on Medicaid alone. Many Arizona retirees with modest assets between $50,000 and $200,000 benefit most from this approach. You can purchase a traditional or hybrid policy in your 50s, use it if needed, and if benefits run out, Medicaid covers remaining costs while the Partnership Program shields remaining assets from recovery.

Understanding these three paths sets the stage for evaluating which option aligns with your health, finances, and goals-a decision that depends heavily on your current age and health status.

How to Choose the Right Long-Term Care Plan for Your Situation

Assess Your Health Status and Family History

Your health status today determines what coverage options remain available to you, and waiting for conditions to improve rarely works in your favor. If you have diabetes, heart disease, or cognitive concerns, traditional long-term care insurance becomes harder to obtain or costs significantly more, assuming underwriters approve you at all. Some insurers require medical exams and prescription drug reviews before issuing policies, which means conditions documented in your medical records directly affect your eligibility and rates. A 60-year-old with hypertension managed by medication might qualify for standard rates, but someone with memory loss or a recent stroke diagnosis could face denial or be steered toward hybrid policies instead.

Family history shapes your timeline considerably. If your parents needed extensive care in their 70s, your own timeline likely compresses, making premiums locked in now substantially cheaper than waiting five more years. The practical step is straightforward: pull your medical records, list any conditions or medications, and obtain preliminary quotes from multiple insurers to see where you actually stand rather than guessing. Arizona retirees often discover they qualify for better rates than they expected, or they learn early that a hybrid policy or Medicaid planning makes more sense than traditional coverage.

Set Benefit Periods and Daily Limits Based on Arizona Costs

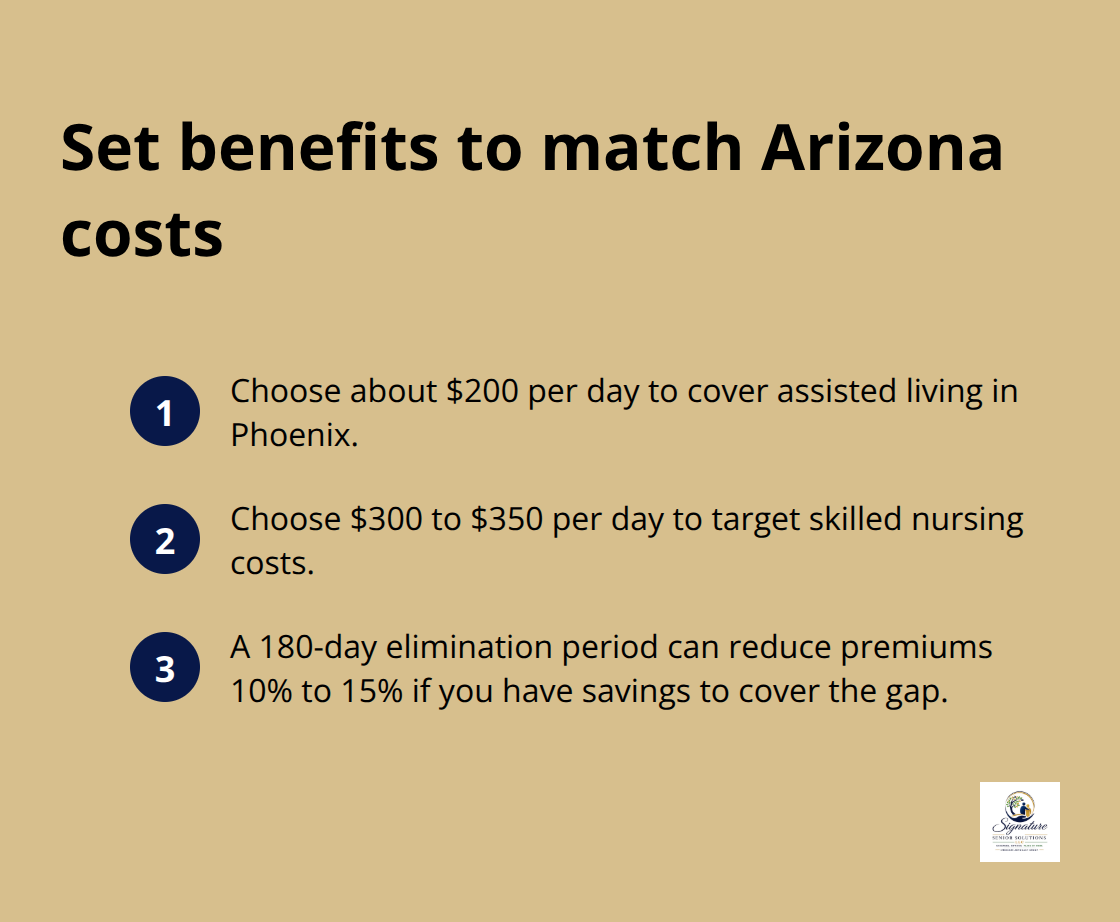

Benefit periods and daily limits directly control how much your policy actually pays when you need care. A $150 daily benefit sounds reasonable until you realize Phoenix assisted living costs slightly over $6,100 monthly, or roughly $200 daily-meaning your policy covers only part of the bill, and you pay the difference. A three-year benefit period ($150 daily) totals roughly $164,250 in lifetime coverage, which sounds substantial until skilled nursing in Tucson hits $10,562 monthly and depletes that pool in just 15 months.

The better approach is working backward from Arizona’s actual costs: if you want coverage for assisted living without personal cost, try a $200 daily benefit; if you want to cover skilled nursing, try $300 to $350 daily. Lifetime or five-year benefits cost more but eliminate the risk of benefits running out mid-care. The elimination period-typically 90 days-affects your premium significantly; choosing a 180-day wait instead of 90 days can cut your monthly cost 10% to 15%, but only if you have liquid savings to cover that gap yourself.

Compare Premium Structures Across Multiple Providers

Comparing premium structures across providers reveals substantial differences. A 55-year-old might pay $1,400 annually with one insurer and $1,800 with another for identical benefits, so obtaining three to five quotes is essential. Age, inflation protection, and whether you choose shared benefits for couples all shift the final number. The National Association of Insurance Commissioners notes that historically 70% to 80% of traditional policyholders faced premium increases, so asking insurers directly about their rate history and whether they experienced major increases in the past decade tells you which companies have kept costs stable.

Arizona’s Rate Stability Rules, based on NAIC guidelines, make rate increases harder than in many states, but increases still happen. Choosing an insurer with a strong track record matters more than saving $200 annually on an initial premium. Request rate history documentation from any insurer you seriously consider, and compare not just current costs but the likelihood that your premium will remain stable over the next 10 to 20 years.

Final Thoughts

Long-term care planning in Arizona demands action now, not later, because costs rise annually and your window to lock in affordable premiums narrows with each passing year. Whether you select traditional long-term care insurance, a hybrid policy, or combine insurance with Medicaid planning through Arizona’s Partnership Program, the decision must reflect your actual health, finances, and family circumstances rather than wishful thinking. Start by obtaining personalized quotes from multiple insurers to discover what coverage costs at your current age and health status-this process takes just an hour or two and immediately clarifies which options remain financially viable for you.

Pull your medical records, list your medications and conditions, and request three to five quotes from different carriers to see how insurers assess your risk profile. You’ll quickly learn whether traditional policies remain affordable or whether hybrid options and Medicaid planning make stronger financial sense for your situation. This information often surprises Arizona retirees and reveals which path forward protects your assets most effectively.

If you’re also evaluating Medicare Supplement plans, vision, dental, or final-expense insurance alongside Arizona long-term care coverage, working with a licensed advisor who understands your state’s specific options prevents costly mistakes and saves considerable time. We at Signature Senior Solutions LLC help Arizona seniors compare and enroll in Medicare Advantage, Part D, Medicare Supplement plans, and complementary coverage like vision, dental, life and final-expense insurance across Maricopa County. Contact us at signaturesenior.solutions to discuss how long-term care insurance fits into your overall retirement protection strategy.

The information provided in this blog is for general informational purposes only and should not be considered legal, tax, financial, healthcare, Medicare, or insurance advice. Medicare plan benefits, premiums, provider networks, drug formularies, eligibility requirements, and availability may vary by carrier and location. Individuals should consult a licensed insurance professional regarding their specific coverage needs and review official Medicare resources before making enrollment decisions.

While we strive to provide accurate and current information, we do not guarantee its completeness or accuracy. Coverage is subject to policy terms, conditions, limitations, and exclusions.

Artificial intelligence may have been used to assist in the creation of text and images contained in this article.